Don’t under estimate the power of compound interest. It can work for you or against you. According to Investopedia the definition of compound interest is: Interest calculated on the initial principal and also on the accumulated interest of previous periods of a deposit or loan. This concept is so powerful that Albert Einstein is said to have called compound interest the “eighth wonder of the world” and that “he who understands it, earns it… he who doesn’t, pays it.” Now, whether Einstein said this or not, it’s a powerful statement nonetheless.

Compound Interest vs Simple Interest:

Most everyone has heard of this concept and it most often comes up when thinking about the growth of savings or investments over the long term. To review, interest can generally be calculated as compound or simple. There is a huge difference so you need to read documents carefully.

Simple interest is calculated by paying or assessing interest only on the original amount. For example, $10,000 is invested and the investment will pay 5% per year simple interest. This means each year, you will be paid $500. This is very similar to the way a bond pays interest.

Now consider compound interest. As stated above, this is where interest is earned or assessed based on the original investment plus the prior years interest. See the chart below for just how major the difference is.

*Rate of return of 5% is for illustration only and is not meant to represent the return of any spefic

Your results will vary. No taxes or fees were included in this calculation. Investing involves risk of

loss and investments are NOT guaranteed or FDIC insured.

[convertkit form=5108043]

Compound Interest: Make It Work For You

It’s important to remember compounding works in reverse and this is where it can work against you. Most likely, if you take out a mortgage, the interest is compounded monthly. When we’re about to make a huge purchase like buying a home, the primary concern is typically the monthly payment and whether or not it fits within our budget. However, even with low interest rates, it can be down right scary how much interest you will have paid over the course of 30 years

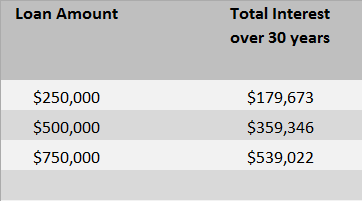

How much interest will you pay? A $250,000 30 year mortgage at 4% will result in a principal and interest payment of $1,193.54 per month. This will cost you $179,673.01 in interest over the 30 years! You will have borrowed $250,000 and paid back $429,673.01. That is a huge number and you can thank compound interest for that. See below for a chart on total interest based on various loan amounts at 4%:

What can you do about it? Use compound interest to your advantage and make it work for you by making small additional payments to principal. Small steps now can make a huge impact down the road. Make the following additional monthly payments at the start of your loan for 15 years and see what happens:

| Additional Payment | Interest Saved | Loan Paid Off |

| $50 | $13,168 | 19 months early |

| $75 | $19,231 | 28 months early |

| $100 | $24,976 | 37 months early |

Make sure you check first with your lender regarding their policy on additional payments and how they’re applied. There are other considerations too. When you make additional payments they are no longer available for other savings which can also utilize compound interest. There are also numerous variations on how and when to apply additional payments to principal for a desired result.

How does compound interest work with investing?

The same concept of compound interest illustrated above applies to investing in stocks, ETFs, and mutual funds. However, the outcome is uncertain due to the variability of returns associated with those types of investments. In general, when you reinvest dividends from stocks, mutual funds, and ETFs, your earnings are compounding.

Let’s say you own 10 shares of XYZ stock and it’s trading at $100 per share. Your total value is $1,000. Now assume XYZ Corp issues a $1 per share dividend to all shareholders. You will receive $10 from XYZ Corp as a dividend. It’s important to note that the share price will drop by the amount of the dividend. Therefore, your stock is now worth $99 for a total value of $990.

You might be wondering where your $10 went. Remember, it was distributed to you via a dividend. When you add the $10 dividend to the new total value of shares owned, you get $1,000. While it may initially seem like you are hurt as a result of the issuance of the dividend, you are in fact made whole when taken together.

Where does compound interest fit in with this?

Many investors choose to reinvest the dividends they receive back into the investment. Most often, all you need to do is notify your advisor or financial institution and they can set it up so it happens automatically. When you reinvest your dividends, you are electing to take the dividend and use it to buy more shares of the stock you own. Let’s get back to the example.

You currently own 10 shares of XYZ stock at $99 per share worth $990 AND you have $10 in cash from the dividend.

Reinvesting the $10 dividend into XYZ stock will cause the purchase of more shares. The $10 purchase of XYZ stock will get you 0.101 shares of stock. You previously owned 10 shares of XYZ and now you own 10.101 shares.

The next time XYZ issues a $1 dividend to shareholders, you will receive $10.10 as a dividend instead of the $10 you received initially. Therefore, as you increase the amount of shares you own with each dividend reinvestment, the amount you receive from each future dividend will increase.

Proceed with caution.

With compound interest on a savings account, interest is paid based on prior interest payments that have been added to the account. With investments like stocks, mutual funds, and ETFs, dividends are paid based on prior dividends that have been reinvested into shares and added to the total shares owned.

Certainly, reinvesting shares into investments doesn’t guarantee that your money with grow. While the total number of shares will grow, the share value will fluctuate and you can lose value. In addition, there is no guarantee that a company will issue future dividends and the amount of dividends can change as well.

Understanding compound interest and making it work for you can save you thousands and thousands of dollars and help you get out of debt quicker. Be smart like Albert Einstein and make compound interest work for you.